Mock Trial: Making the Case for Apple Stock

The evidence keeps mounting that there's an AAPL dip-buying opportunity ahead

My dad is a lawyer. One of his more annoying endearing qualities is that its in his nature as an attorney to be overly thorough. Even the mundane is overexplained as if he’s in court. Legalese like you’ve never seen it before.

Me: Hey is the tree hanging over the side of my yard count as my property or my neighbors?

Fred: Well you see, due to the 1725 Charter on arborist activity, the precedent from Farmer McClellan established the property line vortex. Only until 1965 was it the revoked in Berenstain vs. Bears. Then something weird happened. Farmer Joe, a trailblazer in turf law, argued before the Connecticut Supreme Court against Agway about soil reclamation. So heretofore, escheat states that the tenants right of demurrer goes to the plaintiff.

I would just sit there like:

Arguments with him as a teenager never ended well. I learned to just take the L.

I’ve come to appreciate this the older I got, though. It’s a feature, not a bug. Thorough is good! Thorough leaves no doubt. It’s cool to care about things down to the intricate and often excruciating details. When someone goes in deep like that, its their passion shining through.

Now when my dad does it, it puts a smile on my face. His excitement over the most mundane, unnecessary details is innocence and pride shining through. It warms my heart. It’s even rubbed off on me, without the law degree. My wife has caught me numerous times explaining things five different ways.

I think about that quirk a lot when writing this Substack, even more so six days removed from Father’s Day.

Sometimes, all the data comes together in a way so thorough you could argue the case in front of the Supreme Court. I’ve got one such case right now I’d like to present: Apple (AAPL).

In the beginning, Steve Jobs and Steve Wozniak sold their prized possessions to build their first computer.

Just kidding. But I am going to structure this like a mock trial.

Introduction and Theme

Thank you to the Honorable Judge Market for hearing this case. I’m attorney Patrick Martin, and will be arguing for the plaintiff in the case of Apple (AAPL) v. Bears.

Review of Evidence

Apple is surely not a heavily-shorted, underloved ‘contrarian’ play that’s due for a massive unwinding of pessimism. But one must not fit ‘buy the dip’ plays into just a single rote category. Two timeframes exist right now that feature a bullish case for Apple stock.

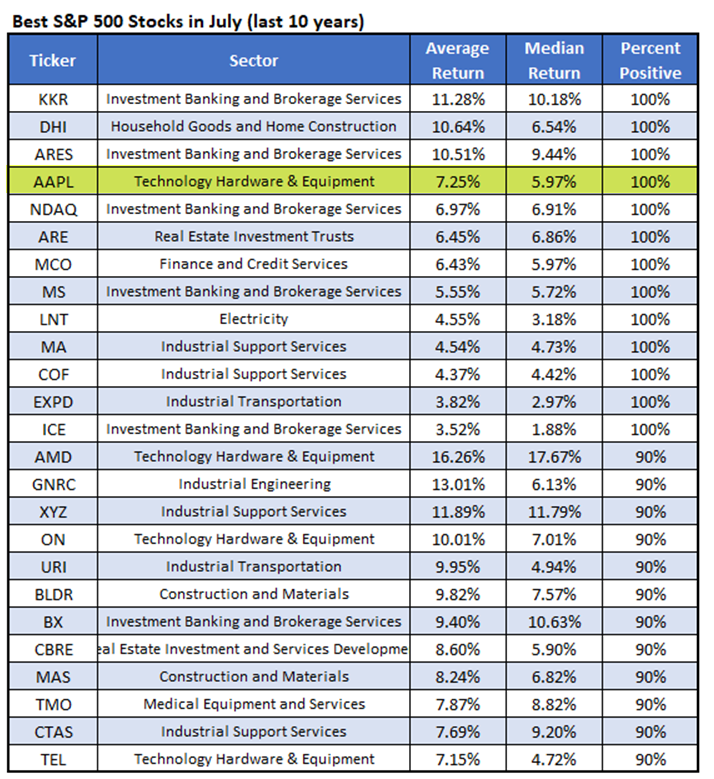

It’s one of the best 25 stocks on the S&P 500 to own in June, historically, looking back 10 years.

A perfect monthly win rate and a healthy 7.3% average July return. Not bad.

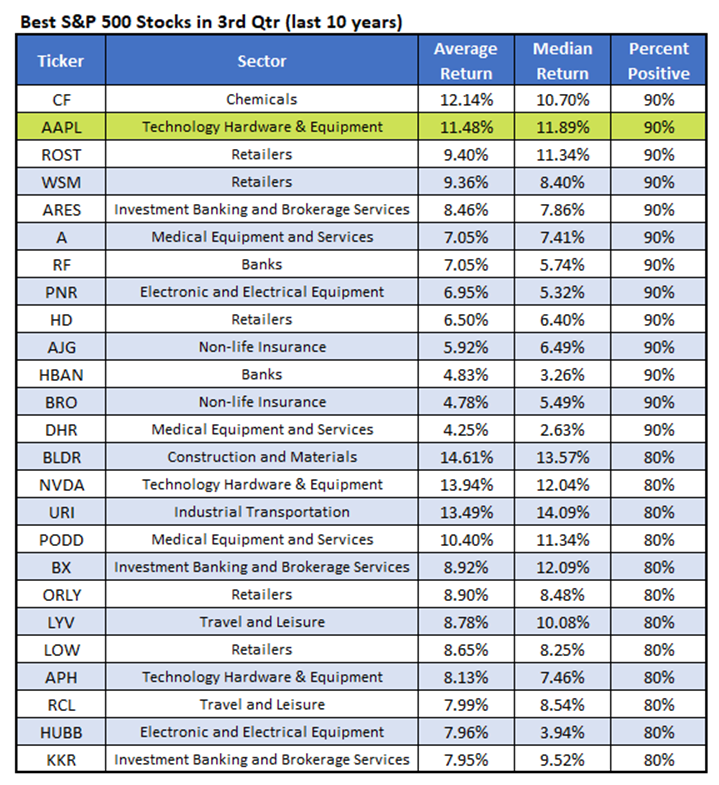

If you wanted a longer timeframe, AAPL is also a Q3 outperformer in the last 10 years.

That average 11.5% return good for fifth best on the table. You’ll note, your honor, that Apple is the only stock appearing on both quantitative lists.

The Prosecution:

Objection! Seasonality is inherently flawed and is not a predicator of future performance. Besides, ladies and gentlemen of the jury, this isn’t some run of the mill pullback. This is a pullback indicative of some troubling macro concerns. Tech stocks have been overvalued for some time now, and this flushing out had to happen.

Read what Ed Zitron has to say about the AI sector and tell me there’s not a bubble. While Apple isn’t the necessarily at the forefront of the AI revolution, they are tangentially impacted. And who knows how sudden and sharp the reckoning could be.

Apple stock shed 4.5% on Thursday, after the company hiked prices on select MacBook and iPad models by roughly $150–$300, citing surging memory and storage chip costs starting to hit margins. No sugarcoating that, it’s less than ideal.

Barring a sharp rally in the next two days, the shares are heading for their worst month since April 2022. AAPL lost 26.8% that year! This nearly 9% monthly drawdown comes after Apple hit a record high of $317.40 on June 8, and could just be the beginning of a precipitous drop.

The Thursday selloff breached round-number $300, the type of psychologically-significant level that raises alarm bells. There’s also the trendline of higher highs that was toppled that indicates a trend reversal.

With short interest up 15.2% in the two most recent reporting period, a continued build of these bearish bets could act as a headwind. Factor in Apple’s lackluster earnings history for its quarterly report on June 30, and there are caution signs aplenty, both macro and micro.

I acknowledge the prosecutions presentation and would like to proceed.

Burden of Proof

If the seasonality study in my opening statement wasn’t enough, let me attack the problem from a different angle.

I believe, your honor, that this is a buying opportunity for Apple. You’ll note in the chart brought forth by the prosecution that the 50-day moving average was tested on Wednesday. Per White’s data, 20 tests of this trendline have occurred in the last decade, after which AAPL averaged a 1.4% gain and 53% win rate.

Nothing eye-opening, I’ll admit. But when stacked with the seasonal evidence above, the bullish case grows. Let’s proceed.

On Thursday, AAPL’s market cap held the $4 trillion level. Yes, round-number levels have a psychological impact on investors, and this could be where the selloff runs out of steam. The chart below shows that once club $4 trillion was reclaimed back in March, it preceded a sharp run up the charts culminating in that early June peak.

You’ll also notice that $280 is the site of former highs from December. History doesn’t repeat, but it does rhyme, and this former resistance-turned support adds to the cushion that could come.

Consider now AAPL’s 14-Day Relative Strength Index (RSI), cratering down to 34.9. The last time the stock was this oversold was March prior to the melt up from the spring.

Before Thursday’s price hike-induced selloff, Apple was in fact a model of resiliency. On Monday, when tech stocks were drubbed, AAPL was the least hit, only shedding 0.3%. While I acknowledge that that relative strength looks a little weaker given Thursday’s selloff when the rest of tech rallied up off the mat, I’m not about to let recency bias cloud the case.

Options traders have a tendency to tip off sentiment. Four of the top six open interest positions are calls, with the August 345 call and July 300 the top two. However, 10-day, the buy-to-open put/call volume ratio of 0.65 sits in the 93rd percentile of its annual range. Calls will almost always rule the roost on an absolute basis, but that rate of put buying at such a high percentile is a layer that must be acknowledged.

Apple will report earnings July 30, and the memory costs are sure to be an overhang to monitor. But in the meantime, I want the record stated for prospective call traders that AAPL implied volatilities call options are near parity with their put counterparts. This is per the stock’s 30-day implied volatility (IV) skew of 7.6%, which registers in the low 10th percentile of its 12-month range.

The Closing Argument

If you’re looking for a dramatic, double-digit pop, life-changing melt-up from Apple, don’t buy the stock. This isn’t some Reddit forum where Wendy’s (WEN) gets pumped. I acknowledge all of the headwinds brought forth by the prosecution. Its disheartening to see AI-driven chip costs passed on to consumers.

The jury may remember my Messi reference last week as it pertains to remarkable consistency. Since 2008, Apple has finished the year lower only three times. It’s up 4.4% in 2026 right now, just barely holding its year-to-date breakeven level.

It’s one of the foundational tech companies of this generation, not some flash-in-the-pan cash grab like SpaceX (SPCX). As we approach the 4th of July, lets remember what this holiday stands for; the enduring power of freedom over tyranny.

There’s nothing more American than buying the dip in the country’s greatest business success stories.